Retirement is not just about stopping work—it’s about ensuring a financially secure and stress-free life. Rising inflation, increasing healthcare costs, and longer life expectancy make smart investment decisions more important than ever.

Senior citizens require investments that offer capital safety, regular income, tax efficiency, liquidity, and inflation protection rather than high-risk wealth creation. The ideal retirement portfolio should balance guaranteed income with moderate long-term growth.

This comprehensive financial guide explains the 11 safest investment options for senior citizens in India for 2026, along with important retirement planning strategies like writing a Will, purchasing adequate health insurance, and maintaining an emergency fund.

Financial Priorities Before Investing

Before investing even a single rupee, every senior citizen should complete these three important tasks.

1. Prepare a Legally Valid Will

A properly drafted Will ensures that your assets reach your legal heirs without unnecessary disputes.

Benefits include:

- Smooth transfer of assets

- Avoidance of family conflicts

- Faster settlement

- Reduced legal complications

A registered Will is always preferable.

2. Buy Adequate Health Insurance

Medical inflation in India is rising rapidly.

Hospitalisation can wipe out years of savings.

Health insurance protects retirement income from unexpected medical expenses.

Avoid purchasing expensive insurance products that combine investment with insurance unless they suit your financial objectives.

3. Maintain an Emergency Fund

Experts recommend maintaining at least 18 months of household expenses in highly liquid investments such as:

- Savings account

- Short-term Fixed Deposits

- Liquid Mutual Funds

This fund should never be used for routine investments.

Top 11 Secure Investment Options for Senior Citizens in 2026

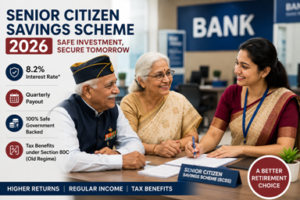

1. Senior Citizen Savings Scheme (SCSS)

Best Overall Government Investment

SCSS continues to remain the first choice for retired individuals.

Key Features

- Interest Rate: Around 8.2% per annum

- Government-backed

- Quarterly interest payment

- Tenure: 5 years (extendable by 3 years)

- Maximum investment as per latest government rules

- Eligible for tax benefits under Section 80C

Suitable For

- Pensioners

- Retired Government Employees

- Defence Veterans

- Individuals seeking guaranteed quarterly income

Pros

✔ Highest safety

✔ Excellent returns

✔ Regular income

✔ Tax benefits

Cons

- Lock-in period

- Interest is taxable

2. RBI Floating Rate Savings Bonds

These bonds are issued by the Reserve Bank of India.

Features

- Current interest approximately 8.05%

- Interest revised every six months

- Government guarantee

- No investment ceiling

- Lock-in period: 7 years

Best For

Investors looking for completely risk-free long-term income.

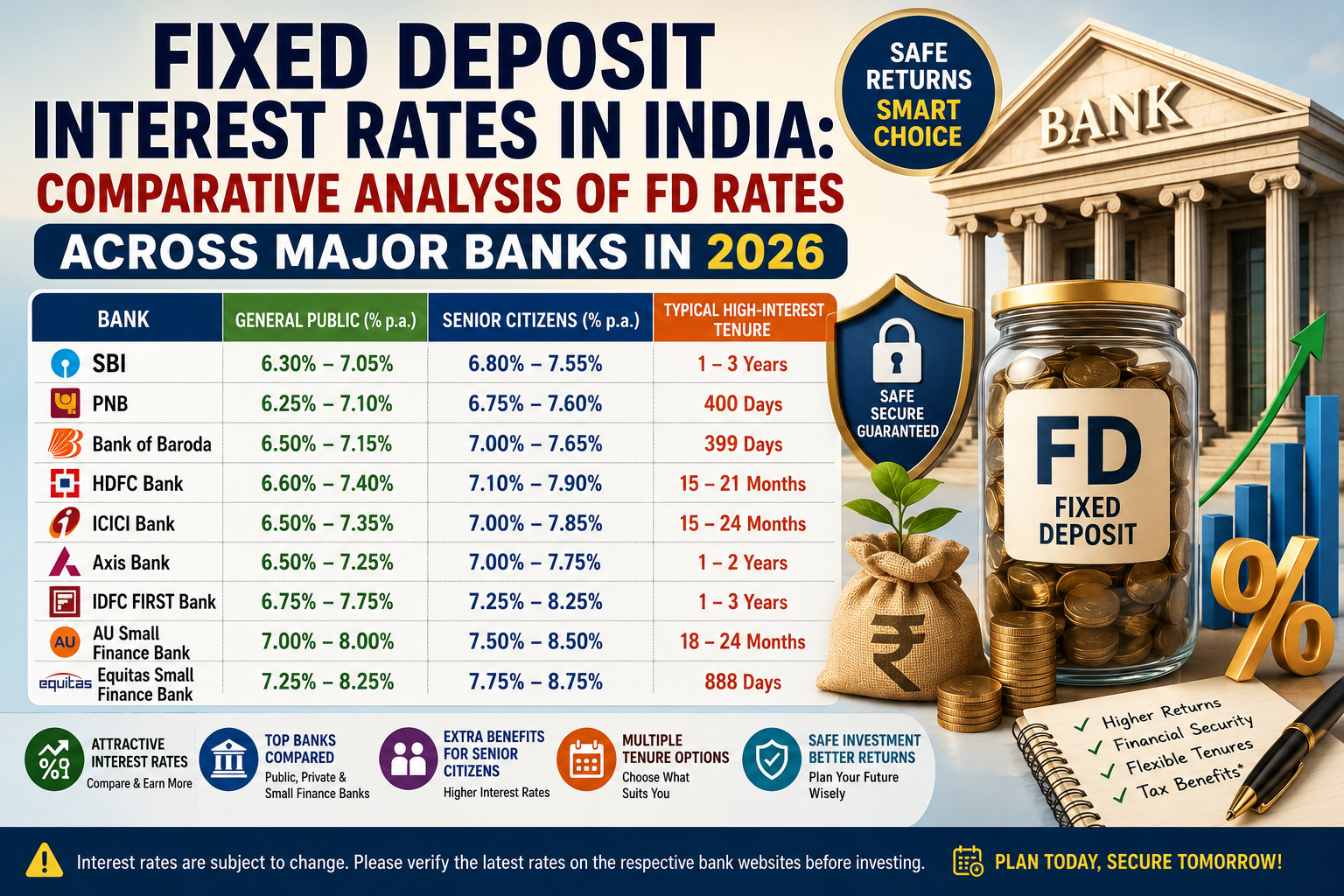

3. Government Bank Fixed Deposits

Public sector banks remain among the safest places to park retirement money.

Examples include:

- SBI

- Bank of Baroda

- Punjab National Bank

- Canara Bank

Interest rates generally range between:

7.0%–7.25%

Advantages include:

- Guaranteed returns

- Flexible tenure

- Premature withdrawal facility

4. Private Bank Fixed Deposits

Well-rated private banks often provide better returns.

Examples include:

- HDFC Bank

- ICICI Bank

- Axis Bank

- DCB Bank

Interest rates may reach:

7.5%–7.85%

Invest only with financially strong banks.

5. Small Finance Bank Fixed Deposits

These banks currently offer among the highest FD rates.

Interest may reach:

8.25%–8.60%

Examples include:

- AU Small Finance Bank

- Equitas

- Jana Small Finance Bank

- Suryoday Small Finance Bank

Safety

Deposits up to ₹5 lakh per depositor per bank are insured by DICGC.

Ideal only if investments are diversified across banks.

6. National Savings Certificate (NSC)

NSC remains a favourite government-backed investment.

Features

- Interest around 7.7%

- Five-year tenure

- Compounded annually

- Tax deduction under Section 80C

Suitable for conservative investors who do not require regular monthly income.

7. Post Office Monthly Income Scheme (POMIS)

Ideal for retirees seeking monthly cash flow.

Features

- Interest approximately 7.4%

- Monthly income

- Government-backed

- Individual and joint accounts available

Excellent for meeting routine household expenses.

8. Kisan Vikas Patra (KVP)

A completely secure investment from India Post.

Features

- Interest approximately 7.5%

- Money doubles over the prescribed maturity period

- Government guarantee

Suitable for long-term investors.

9. Post Office Time Deposit (POTD)

Post Office Time Deposits offer safety comparable to bank FDs.

Current interest varies with tenure.

- 1 Year

- 2 Year

- 3 Year

- 5 Year

Benefits include:

- Government security

- Guaranteed returns

- Tax benefits on 5-year deposits

10. Gold (Physical, ETF or Sovereign Alternatives)

Gold should not dominate a retirement portfolio.

Experts generally recommend allocating only 10–15% of total investments.

Gold protects wealth against:

- Inflation

- Currency depreciation

- Global economic uncertainty

Gold ETFs and Gold Mutual Funds eliminate storage risks associated with physical gold.

11. Hybrid Mutual Funds & Large Cap Mutual Funds

Senior citizens with moderate risk tolerance may allocate a limited portion of their portfolio to mutual funds.

Preferred categories:

- Hybrid Funds

- Balanced Advantage Funds

- Large Cap Index Funds

Avoid excessive allocation to:

- Small Cap Funds

- Sectoral Funds

- Thematic Funds

Suggested allocation:

10–20% depending on financial goals.

These investments provide long-term growth and help beat inflation.

Sample Retirement Portfolio (Illustrative)

| Investment | Suggested Allocation |

| SCSS | 25% |

| RBI Bonds | 20% |

| Fixed Deposits | 20% |

| Post Office Schemes | 15% |

| Gold | 10% |

| Hybrid Mutual Funds | 10% |

Actual allocation should depend on age, pension income, health, and financial goals.

Tax Planning Tips for Senior Citizens

Some important tax-saving provisions include:

- Deduction on interest income under Section 80TTB.

- Tax benefits under Section 80C for eligible investments like SCSS and NSC.

- Consider spreading investments across financial years to optimise tax liability.

- Keep Form 15H updated if eligible to avoid unnecessary TDS.

Consult a qualified tax professional for personalised advice.

Investment Mistakes Senior Citizens Should Avoid

❌ Investing everything in one bank

❌ Chasing unusually high interest rates

❌ Buying complex insurance-cum-investment products without understanding them

❌ Ignoring inflation

❌ Keeping nominees outdated

❌ Not writing a Will

❌ Investing emergency funds in long lock-in products

❌ Falling victim to online investment scams and fraudulent schemes promising unrealistic returns

How to Build a Safe Retirement Portfolio

A balanced retirement strategy should combine:

- Guaranteed income

- Government-backed investments

- Bank deposits

- Limited equity exposure

- Gold as an inflation hedge

- Emergency liquidity

- Tax-efficient planning

- Proper estate planning

This diversified approach helps preserve wealth while generating stable income throughout retirement.

Frequently Asked Questions (FAQs)

Which is the safest investment for senior citizens in 2026?

The Senior Citizen Savings Scheme (SCSS) remains one of the safest and most rewarding government-backed investment options.

Which investment gives monthly income?

The Post Office Monthly Income Scheme (POMIS) is specifically designed to provide regular monthly income.

Should senior citizens invest in mutual funds?

Yes, but only a limited allocation to Hybrid or Large Cap Mutual Funds is generally appropriate for those with moderate risk tolerance and long investment horizons.

How much emergency fund should retirees maintain?

A reserve covering approximately 18 months of living expenses is commonly recommended to handle medical and unforeseen emergencies.

Is gold a good investment after retirement?

Gold can serve as an inflation hedge and portfolio diversifier, but it is generally advisable to limit exposure to about 10–15% of total investments.

Final Thoughts

Financial security after retirement depends not on chasing the highest returns but on building a diversified portfolio that balances safety, income, liquidity, and inflation protection. Government-backed schemes like the Senior Citizen Savings Scheme, RBI Floating Rate Bonds, and Post Office savings products provide dependable returns, while a measured allocation to gold and hybrid mutual funds can help preserve purchasing power over the long term.

Equally important are non-investment decisions—maintaining adequate health insurance, preparing a legally valid Will, updating nominees, and keeping an emergency fund. Together, these steps create a strong financial foundation, helping senior citizens enjoy a comfortable and worry-free retirement while protecting their families from avoidable legal and financial challenges.

- Senior Citizens Savings Scheme (SCSS) in Post Office 2026: Complete Guide, Interest Rate, Eligibility, Tax Benefits & ₹30 Lakh Interest Calculation

Senior Citizens Savings Scheme (SCSS): The Best Government Investment Scheme for… Read more: Senior Citizens Savings Scheme (SCSS) in Post Office 2026: Complete Guide, Interest Rate, Eligibility, Tax Benefits & ₹30 Lakh Interest Calculation

Senior Citizens Savings Scheme (SCSS): The Best Government Investment Scheme for… Read more: Senior Citizens Savings Scheme (SCSS) in Post Office 2026: Complete Guide, Interest Rate, Eligibility, Tax Benefits & ₹30 Lakh Interest Calculation - Fixed Deposit Interest Rates in India August 2026 : Which Bank Offers the Best Returns?

Fixed Deposits (FDs) continue to remain one of the most popular… Read more: Fixed Deposit Interest Rates in India August 2026 : Which Bank Offers the Best Returns?

Fixed Deposits (FDs) continue to remain one of the most popular… Read more: Fixed Deposit Interest Rates in India August 2026 : Which Bank Offers the Best Returns? - How to Become Rich with Your Present Income : The Secret Guide to Smart Investing and Wealth Creation

How to Become Rich with Your Potential and Present Income: Investing… Read more: How to Become Rich with Your Present Income : The Secret Guide to Smart Investing and Wealth Creation

How to Become Rich with Your Potential and Present Income: Investing… Read more: How to Become Rich with Your Present Income : The Secret Guide to Smart Investing and Wealth Creation - The Master Guide to Systematic Withdrawal Plans (SWP): Build a Reliable Monthly Income from Mutual Funds

Systematic Withdrawal Plans (SWPs) have become one of the most effective… Read more: The Master Guide to Systematic Withdrawal Plans (SWP): Build a Reliable Monthly Income from Mutual Funds

Systematic Withdrawal Plans (SWPs) have become one of the most effective… Read more: The Master Guide to Systematic Withdrawal Plans (SWP): Build a Reliable Monthly Income from Mutual Funds - Post Office Small Savings Interest Revised Rates from 1 July 2026: Compare with Bank FD & other Investment Options

The Government of India has retained the interest rates on all… Read more: Post Office Small Savings Interest Revised Rates from 1 July 2026: Compare with Bank FD & other Investment Options

The Government of India has retained the interest rates on all… Read more: Post Office Small Savings Interest Revised Rates from 1 July 2026: Compare with Bank FD & other Investment Options - 95% People Don’t Know This Government Investment That Offers High Returns and Maximum Safety – Complete Guide to India Post Savings Schemes 2026

Looking for a completely safe investment that provides better returns than… Read more: 95% People Don’t Know This Government Investment That Offers High Returns and Maximum Safety – Complete Guide to India Post Savings Schemes 2026

Looking for a completely safe investment that provides better returns than… Read more: 95% People Don’t Know This Government Investment That Offers High Returns and Maximum Safety – Complete Guide to India Post Savings Schemes 2026 - Invest in Corporate Bonds with Up to 13.25% Returns: A Smart and safe Investment Option for Stable Income for Pensioners

Invest in Corporate Bonds with Up to 13.25% Returns: Complete Guide… Read more: Invest in Corporate Bonds with Up to 13.25% Returns: A Smart and safe Investment Option for Stable Income for Pensioners

Invest in Corporate Bonds with Up to 13.25% Returns: Complete Guide… Read more: Invest in Corporate Bonds with Up to 13.25% Returns: A Smart and safe Investment Option for Stable Income for Pensioners - How to Invest Your ₹1 Crore Retirement Corpus Wisely in India (2026 Guide): The Complete Safe Investment Roadmap for Lifelong Monthly Income

How to Invest Your ₹1 Crore Retirement Corpus Wisely Without Losing… Read more: How to Invest Your ₹1 Crore Retirement Corpus Wisely in India (2026 Guide): The Complete Safe Investment Roadmap for Lifelong Monthly Income

How to Invest Your ₹1 Crore Retirement Corpus Wisely Without Losing… Read more: How to Invest Your ₹1 Crore Retirement Corpus Wisely in India (2026 Guide): The Complete Safe Investment Roadmap for Lifelong Monthly Income - Senior Citizen Savings Scheme (SCSS) 2026: Complete Guide to Interest Rate, Eligibility, Tax Benefits, Withdrawal Rules & Smart Investment Strategy

Senior Citizen Savings Scheme (SCSS) 2026: A Safe Investment for Regular… Read more: Senior Citizen Savings Scheme (SCSS) 2026: Complete Guide to Interest Rate, Eligibility, Tax Benefits, Withdrawal Rules & Smart Investment Strategy

Senior Citizen Savings Scheme (SCSS) 2026: A Safe Investment for Regular… Read more: Senior Citizen Savings Scheme (SCSS) 2026: Complete Guide to Interest Rate, Eligibility, Tax Benefits, Withdrawal Rules & Smart Investment Strategy - Business Wisdom for Exservicemen and Fresher Beginners : Business Case Studies Every Entrepreneur Must Learn Before Starting a Business

Introduction A large number of Ex-servicemen are intended to establish their… Read more: Business Wisdom for Exservicemen and Fresher Beginners : Business Case Studies Every Entrepreneur Must Learn Before Starting a Business

Introduction A large number of Ex-servicemen are intended to establish their… Read more: Business Wisdom for Exservicemen and Fresher Beginners : Business Case Studies Every Entrepreneur Must Learn Before Starting a Business - Top 11 Secure Investment Options for Senior Citizens & Exservicemen in 2026: A Complete Financial Guide for Safe Income & Wealth Protection

Retirement is not just about stopping work—it’s about ensuring a financially… Read more: Top 11 Secure Investment Options for Senior Citizens & Exservicemen in 2026: A Complete Financial Guide for Safe Income & Wealth Protection

Retirement is not just about stopping work—it’s about ensuring a financially… Read more: Top 11 Secure Investment Options for Senior Citizens & Exservicemen in 2026: A Complete Financial Guide for Safe Income & Wealth Protection - Warren Buffett’s 7 Golden Rules of Investing: The Ultimate Beginner-to-Advanced Roadmap for Safe Wealth Creation

What are the kind of investors ? Every market cycle creates… Read more: Warren Buffett’s 7 Golden Rules of Investing: The Ultimate Beginner-to-Advanced Roadmap for Safe Wealth Creation

What are the kind of investors ? Every market cycle creates… Read more: Warren Buffett’s 7 Golden Rules of Investing: The Ultimate Beginner-to-Advanced Roadmap for Safe Wealth Creation - Best Investment Plan in 2026 for a Better Life: A Complete Guide to Building Wealth and Financial Security

Money alone cannot guarantee happiness, but poor financial planning can certainly… Read more: Best Investment Plan in 2026 for a Better Life: A Complete Guide to Building Wealth and Financial Security

Money alone cannot guarantee happiness, but poor financial planning can certainly… Read more: Best Investment Plan in 2026 for a Better Life: A Complete Guide to Building Wealth and Financial Security - 2026 Investment Caution: Amid the Iran–Israel–US Crisis What Government Employees, Pensioners and Small Savers Must Know

Global Uncertainty Returns: Why Investors Need to be Careful in 2026… Read more: 2026 Investment Caution: Amid the Iran–Israel–US Crisis What Government Employees, Pensioners and Small Savers Must Know

Global Uncertainty Returns: Why Investors Need to be Careful in 2026… Read more: 2026 Investment Caution: Amid the Iran–Israel–US Crisis What Government Employees, Pensioners and Small Savers Must Know - Fixed Deposits vs Mutual Funds: The Compounding Advantage Explained for Government Employees, Pensioners and Small Savers (2026 Guide)

FD vs Mutual Fund : Which One Creates More Wealth in… Read more: Fixed Deposits vs Mutual Funds: The Compounding Advantage Explained for Government Employees, Pensioners and Small Savers (2026 Guide)

FD vs Mutual Fund : Which One Creates More Wealth in… Read more: Fixed Deposits vs Mutual Funds: The Compounding Advantage Explained for Government Employees, Pensioners and Small Savers (2026 Guide) - Invest in Bitcoin SIP Safe in 2026? Reality Check, Risks, Returns and Smart Investment Strategy for Indian Investors

Bitcoin SIP in 2026: Can It Really Make You Rich? Over… Read more: Invest in Bitcoin SIP Safe in 2026? Reality Check, Risks, Returns and Smart Investment Strategy for Indian Investors

Bitcoin SIP in 2026: Can It Really Make You Rich? Over… Read more: Invest in Bitcoin SIP Safe in 2026? Reality Check, Risks, Returns and Smart Investment Strategy for Indian Investors - How to Get the Best Returns from Post Office Investments in 2026: Smart Strategies to Earn Up to 9.75% Safely

When it comes to safe and guaranteed investments in India, Post… Read more: How to Get the Best Returns from Post Office Investments in 2026: Smart Strategies to Earn Up to 9.75% Safely

When it comes to safe and guaranteed investments in India, Post… Read more: How to Get the Best Returns from Post Office Investments in 2026: Smart Strategies to Earn Up to 9.75% Safely - Check this Before Start SIP for MF in 2026 : 5 Best Mutual Funds In Last 5 Years

Mutual fund investing has become one of the most effective wealth… Read more: Check this Before Start SIP for MF in 2026 : 5 Best Mutual Funds In Last 5 Years

Mutual fund investing has become one of the most effective wealth… Read more: Check this Before Start SIP for MF in 2026 : 5 Best Mutual Funds In Last 5 Years - Stock Market Investment for Government Employees and Pensioners: Eligibility, Rules and Tips

Concept of Invetment in Stock Market for Govt Employees and Pensioners… Read more: Stock Market Investment for Government Employees and Pensioners: Eligibility, Rules and Tips

Concept of Invetment in Stock Market for Govt Employees and Pensioners… Read more: Stock Market Investment for Government Employees and Pensioners: Eligibility, Rules and Tips - 60 Years Old with No Retirement Savings? Here’s How You Can Still Build Financial Security

Turning 60 with little or no retirement savings can feel frightening.… Read more: 60 Years Old with No Retirement Savings? Here’s How You Can Still Build Financial Security

Turning 60 with little or no retirement savings can feel frightening.… Read more: 60 Years Old with No Retirement Savings? Here’s How You Can Still Build Financial Security