FD vs Mutual Fund : Which One Creates More Wealth in the Long Run?

For decades, Indian families, government employees, defence pensioners, and senior citizens have trusted Fixed Deposits (FDs) as the safest way to save money. The guarantee of capital protection and assured returns provides peace of mind. However, a major question is emerging in 2026:

Can Fixed Deposits really help you build wealth after inflation and taxes?

With increasing life expectancy, rising healthcare expenses, and the growing cost of living, investors now need to think beyond merely saving money. They need a strategy for wealth creation. This is where the debate between Fixed Deposits (FDs) and Mutual Funds (MFs) becomes important.

Understanding the Power of Compounding

Albert Einstein reportedly called compounding the “eighth wonder of the world.” Compounding means: You earn returns not only on your original investment but also on the returns already generated. Over long periods, compounding creates exponential wealth growth.

Example: ₹5 Lakh Investment

| Investment | Return Rate | Doubling Time |

|---|---|---|

| FD | 7% | About 10 years |

| Mutual Fund | 14% | About 5 years |

Using the Rule of 72 : 72 ÷ Interest Rate = Approximate Doubling Period

- 72 ÷ 7 = 10.3 years

- 72 ÷ 14 = 5.1 years

The 20-Year Wealth Creation Comparison

Suppose you invest ₹5 lakh and never touch it.

Fixed Deposit at 7%

- Year 0 = ₹5 lakh

- Year 10 = ₹10 lakh

- Year 20 = ₹20 lakh

Mutual Fund at 14%

- Year 0 = ₹5 lakh

- Year 5 = ₹10 lakh

- Year 10 = ₹20 lakh

- Year 15 = ₹40 lakh

- Year 20 = ₹80 lakh

Result

| Investment | Value After 20 Years |

|---|---|

| FD | ₹20 lakh |

| Mutual Fund | ₹80 lakh |

Difference: ₹60 lakh

This is the real power of compounding. Even though the return rate is only double (14% vs 7%), the final wealth becomes four times larger due to faster compounding.

The Silent Enemy: Inflation

Many investors celebrate earning 7% on an FD. But what if inflation is 6%? Your real return becomes : 7% – 6% = 1%

After taxes, the real return can become even lower. Many investors underestimate how inflation gradually reduces purchasing power over 10–20 years. Discussions among investors frequently highlight that preserving capital alone is not enough; preserving purchasing power matters equally.

Example

A medical expense costing ₹1 lakh today may cost ₹3–4 lakh after 20 years. Your money must grow faster than inflation.

Why Government Employees Should Understand This Difference

Government employees already enjoy relatively stable income streams through:

- Salary

- EPF/GPF

- NPS or UPS

- Pension benefits (for eligible retirees)

Therefore, they often have a higher ability to take calculated long-term investment exposure than individuals without retirement support. A young government employee aged 30 has:

- 25–30 years before retirement

- Regular monthly income

- Time to recover from market volatility

This makes mutual funds particularly powerful for retirement wealth creation.

Why Pensioners Need a Different Strategy

Pensioners have different priorities. They need:

Income Stability

- Monthly expenses

- Medical costs

- Emergency liquidity

Capital Protection

A retired person cannot wait 15 years for market recovery if funds are needed immediately.

Therefore pensioners should generally prefer a mix of:

- FDs

- Senior Citizens Savings Scheme (SCSS)

- Post Office schemes

- Limited mutual fund allocation

SCSS currently offers 8.2% and provides government-backed income security, making it attractive for retirees seeking predictable cash flow.

The Biggest Risk in Mutual Funds

Mutual funds are market-linked. Unlike FDs:

- Returns are not guaranteed.

- Values fluctuate daily.

- Short-term losses are possible.

Example

You invest ₹5 lakh. During a market correction:

- Value may fall to ₹4.60 lakh.

- Panic selling locks in the loss.

This is the biggest mistake made by first-time investors.

Why Most Long-Term Investors Still Prefer SIPs

A SIP (Systematic Investment Plan) allows investing a fixed amount every month.

Example:

- ₹500/month

- ₹1,000/month

- ₹5,000/month

No large investment is required.

SIPs automatically use Rupee Cost Averaging, meaning you buy more units when prices are low and fewer when prices are high. This helps reduce timing risk and encourages disciplined investing.

Benefits of Starting a Small SIP

Many people believe wealth creation requires lakhs of rupees. That is false.

A Beginner Can Start With

- ₹500

- ₹1,000

- ₹2,000 per month

Benefits include:

1. Financial Discipline

Regular investing becomes a habit.

2. Lower Timing Risk

You do not need to predict market highs and lows.

3. Compounding Starts Early

Time matters more than amount.

4. Easy for Government Employees

Monthly salary aligns perfectly with SIP investing.

5. Wealth Creation Potential

Even modest SIPs can accumulate substantial retirement wealth over long periods when combined with discipline and periodic increases.

Why You Should Not Stop SIPs During Market Crashes

Many investors stop SIPs when markets fall. This is usually the wrong decision. When markets decline:

- NAV becomes cheaper.

- SIP buys more units.

- Future recovery becomes more rewarding.

Investor education resources consistently note that SIP discipline and continued investing during downturns are key contributors to long-term wealth creation.

When Should You Choose Fixed Deposits?

FDs are ideal when: Goal Period is Less Than 3 Years

Examples:

- Marriage expenses

- Vehicle purchase

- Home renovation

- Emergency fund

Capital Safety is Most Important

Suitable for:

- Senior citizens

- Pensioners

- Risk-averse investors

Income Certainty is Required

You know exactly how much money you will receive.

When Should You Choose Mutual Funds?

Mutual funds are ideal when:

Goal Period is More Than 10 Years

Examples :

- Retirement planning

- Child education

- Wealth creation

- Financial independence

You Can Tolerate Volatility

Markets may fluctuate but historically reward patience over long horizons.

Inflation Protection Matters

Equity-oriented investments have generally provided stronger long-term inflation-beating potential than traditional deposits. (Reddit)

Taxation Comparison in 2026

Fixed Deposits

- Interest taxed as per income tax slab.

- TDS may apply.

- Higher tax bracket investors often lose a significant portion of returns.

Mutual Funds

- Tax applies mainly when units are redeemed or sold.

- Tax treatment varies between equity, debt, and hybrid funds.

- Holding period affects taxation.

Always evaluate post-tax returns, not just advertised returns.

Goal-Based Investment Strategy

Emergency Fund

100% FD or Savings Account

Goal Within 1–3 Years

70–100% FD

Goal Within 3–5 Years

Combination of:

- FD

- Debt Mutual Fund

- Hybrid Funds

Goal Beyond 10 Years

Primarily:

- Equity Mutual Funds

- SIPs

Ideal Asset Allocation for Different Investors

Young Government Employee (Age 25–40)

- 20% FD

- 80% Mutual Funds

Mid-Career Government Employee (Age 40–55)

- 40% FD

- 60% Mutual Funds

Pensioner (Age 60+)

- 70–80% Safe Instruments

- 20–30% Mutual Funds

Allocation should always be adjusted according to personal risk tolerance and income needs.

Common Mistakes to Avoid

Investing Entire Savings in FDs

May fail to beat inflation.

Investing Entire Savings in Equity Funds

Creates excessive risk.

Withdrawing Mutual Funds During Market Crashes

Locks in losses.

Stopping SIPs During Corrections

Destroys compounding benefits.

Chasing High Returns

Focus on goals, not headlines.

Final Verdict: FD or Mutual Fund?

The answer is not FD vs Mutual Fund.

The smarter answer is FD + Mutual Fund.

Use FDs For:

Emergency funds

Short-term goals

Retirement income stability

Capital protection

Use Mutual Funds For:

Long-term wealth creation

Retirement corpus building

Inflation-beating growth

Financial independence

For government employees, defence personnel, pensioners, and small savers, the most successful strategy is usually a balanced portfolio where FDs provide safety and mutual funds provide growth.

Remember:

Fixed Deposits protect your money.

Mutual Funds help your money grow.

Wealth is created when safety and growth work together.

Investment Disclaimer: Mutual Fund investments are subject to market risks. Past performance does not guarantee future returns. Investors should assess their risk profile and financial goals or consult a SEBI-registered investment adviser before investing.

- Senior Citizens Savings Scheme (SCSS) in Post Office 2026: Complete Guide, Interest Rate, Eligibility, Tax Benefits & ₹30 Lakh Interest Calculation

Senior Citizens Savings Scheme (SCSS): The Best Government Investment Scheme… Read more: Senior Citizens Savings Scheme (SCSS) in Post Office 2026: Complete Guide, Interest Rate, Eligibility, Tax Benefits & ₹30 Lakh Interest Calculation

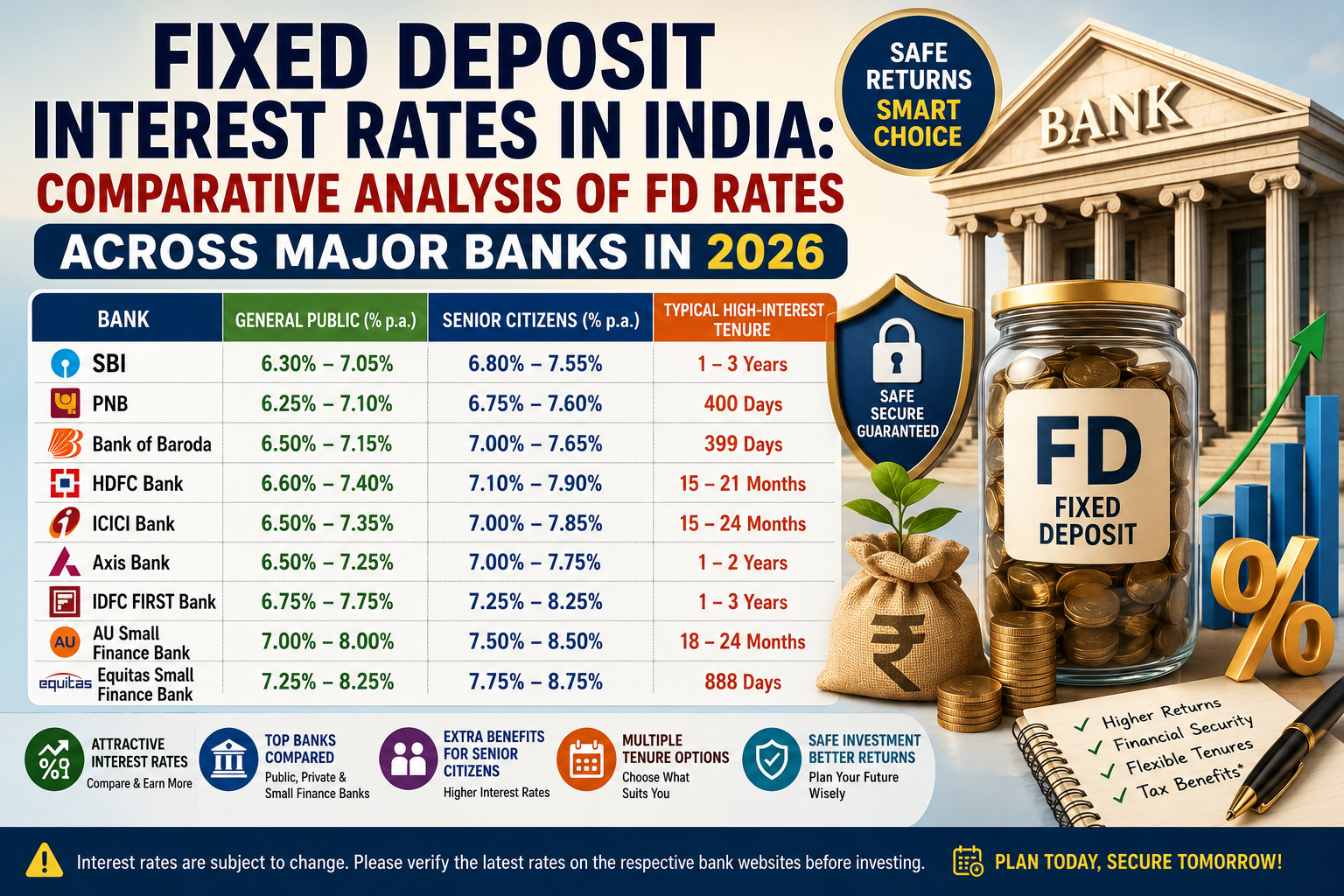

Senior Citizens Savings Scheme (SCSS): The Best Government Investment Scheme… Read more: Senior Citizens Savings Scheme (SCSS) in Post Office 2026: Complete Guide, Interest Rate, Eligibility, Tax Benefits & ₹30 Lakh Interest Calculation - Fixed Deposit Interest Rates in India August 2026 : Which Bank Offers the Best Returns?

Fixed Deposits (FDs) continue to remain one of the most… Read more: Fixed Deposit Interest Rates in India August 2026 : Which Bank Offers the Best Returns?

Fixed Deposits (FDs) continue to remain one of the most… Read more: Fixed Deposit Interest Rates in India August 2026 : Which Bank Offers the Best Returns? - How to Become Rich with Your Present Income : The Secret Guide to Smart Investing and Wealth Creation

How to Become Rich with Your Potential and Present Income:… Read more: How to Become Rich with Your Present Income : The Secret Guide to Smart Investing and Wealth Creation

How to Become Rich with Your Potential and Present Income:… Read more: How to Become Rich with Your Present Income : The Secret Guide to Smart Investing and Wealth Creation - The Master Guide to Systematic Withdrawal Plans (SWP): Build a Reliable Monthly Income from Mutual Funds

Systematic Withdrawal Plans (SWPs) have become one of the most… Read more: The Master Guide to Systematic Withdrawal Plans (SWP): Build a Reliable Monthly Income from Mutual Funds

Systematic Withdrawal Plans (SWPs) have become one of the most… Read more: The Master Guide to Systematic Withdrawal Plans (SWP): Build a Reliable Monthly Income from Mutual Funds - Post Office Small Savings Interest Revised Rates from 1 July 2026: Compare with Bank FD & other Investment Options

The Government of India has retained the interest rates on… Read more: Post Office Small Savings Interest Revised Rates from 1 July 2026: Compare with Bank FD & other Investment Options

The Government of India has retained the interest rates on… Read more: Post Office Small Savings Interest Revised Rates from 1 July 2026: Compare with Bank FD & other Investment Options - 95% People Don’t Know This Government Investment That Offers High Returns and Maximum Safety – Complete Guide to India Post Savings Schemes 2026

Looking for a completely safe investment that provides better returns… Read more: 95% People Don’t Know This Government Investment That Offers High Returns and Maximum Safety – Complete Guide to India Post Savings Schemes 2026

Looking for a completely safe investment that provides better returns… Read more: 95% People Don’t Know This Government Investment That Offers High Returns and Maximum Safety – Complete Guide to India Post Savings Schemes 2026 - Invest in Corporate Bonds with Up to 13.25% Returns: A Smart and safe Investment Option for Stable Income for Pensioners

Invest in Corporate Bonds with Up to 13.25% Returns: Complete… Read more: Invest in Corporate Bonds with Up to 13.25% Returns: A Smart and safe Investment Option for Stable Income for Pensioners

Invest in Corporate Bonds with Up to 13.25% Returns: Complete… Read more: Invest in Corporate Bonds with Up to 13.25% Returns: A Smart and safe Investment Option for Stable Income for Pensioners - How to Invest Your ₹1 Crore Retirement Corpus Wisely in India (2026 Guide): The Complete Safe Investment Roadmap for Lifelong Monthly Income

How to Invest Your ₹1 Crore Retirement Corpus Wisely Without… Read more: How to Invest Your ₹1 Crore Retirement Corpus Wisely in India (2026 Guide): The Complete Safe Investment Roadmap for Lifelong Monthly Income

How to Invest Your ₹1 Crore Retirement Corpus Wisely Without… Read more: How to Invest Your ₹1 Crore Retirement Corpus Wisely in India (2026 Guide): The Complete Safe Investment Roadmap for Lifelong Monthly Income - Senior Citizen Savings Scheme (SCSS) 2026: Complete Guide to Interest Rate, Eligibility, Tax Benefits, Withdrawal Rules & Smart Investment Strategy

Senior Citizen Savings Scheme (SCSS) 2026: A Safe Investment for… Read more: Senior Citizen Savings Scheme (SCSS) 2026: Complete Guide to Interest Rate, Eligibility, Tax Benefits, Withdrawal Rules & Smart Investment Strategy

Senior Citizen Savings Scheme (SCSS) 2026: A Safe Investment for… Read more: Senior Citizen Savings Scheme (SCSS) 2026: Complete Guide to Interest Rate, Eligibility, Tax Benefits, Withdrawal Rules & Smart Investment Strategy - Business Wisdom for Exservicemen and Fresher Beginners : Business Case Studies Every Entrepreneur Must Learn Before Starting a Business

Introduction A large number of Ex-servicemen are intended to establish… Read more: Business Wisdom for Exservicemen and Fresher Beginners : Business Case Studies Every Entrepreneur Must Learn Before Starting a Business

Introduction A large number of Ex-servicemen are intended to establish… Read more: Business Wisdom for Exservicemen and Fresher Beginners : Business Case Studies Every Entrepreneur Must Learn Before Starting a Business - Top 11 Secure Investment Options for Senior Citizens & Exservicemen in 2026: A Complete Financial Guide for Safe Income & Wealth Protection

Retirement is not just about stopping work—it’s about ensuring a… Read more: Top 11 Secure Investment Options for Senior Citizens & Exservicemen in 2026: A Complete Financial Guide for Safe Income & Wealth Protection

Retirement is not just about stopping work—it’s about ensuring a… Read more: Top 11 Secure Investment Options for Senior Citizens & Exservicemen in 2026: A Complete Financial Guide for Safe Income & Wealth Protection - Warren Buffett’s 7 Golden Rules of Investing: The Ultimate Beginner-to-Advanced Roadmap for Safe Wealth Creation

What are the kind of investors ? Every market cycle… Read more: Warren Buffett’s 7 Golden Rules of Investing: The Ultimate Beginner-to-Advanced Roadmap for Safe Wealth Creation

What are the kind of investors ? Every market cycle… Read more: Warren Buffett’s 7 Golden Rules of Investing: The Ultimate Beginner-to-Advanced Roadmap for Safe Wealth Creation - Best Investment Plan in 2026 for a Better Life: A Complete Guide to Building Wealth and Financial Security

Money alone cannot guarantee happiness, but poor financial planning can… Read more: Best Investment Plan in 2026 for a Better Life: A Complete Guide to Building Wealth and Financial Security

Money alone cannot guarantee happiness, but poor financial planning can… Read more: Best Investment Plan in 2026 for a Better Life: A Complete Guide to Building Wealth and Financial Security - 2026 Investment Caution: Amid the Iran–Israel–US Crisis What Government Employees, Pensioners and Small Savers Must Know

Global Uncertainty Returns: Why Investors Need to be Careful in… Read more: 2026 Investment Caution: Amid the Iran–Israel–US Crisis What Government Employees, Pensioners and Small Savers Must Know

Global Uncertainty Returns: Why Investors Need to be Careful in… Read more: 2026 Investment Caution: Amid the Iran–Israel–US Crisis What Government Employees, Pensioners and Small Savers Must Know - Fixed Deposits vs Mutual Funds: The Compounding Advantage Explained for Government Employees, Pensioners and Small Savers (2026 Guide)

FD vs Mutual Fund : Which One Creates More Wealth… Read more: Fixed Deposits vs Mutual Funds: The Compounding Advantage Explained for Government Employees, Pensioners and Small Savers (2026 Guide)

FD vs Mutual Fund : Which One Creates More Wealth… Read more: Fixed Deposits vs Mutual Funds: The Compounding Advantage Explained for Government Employees, Pensioners and Small Savers (2026 Guide) - Invest in Bitcoin SIP Safe in 2026? Reality Check, Risks, Returns and Smart Investment Strategy for Indian Investors

Bitcoin SIP in 2026: Can It Really Make You Rich?… Read more: Invest in Bitcoin SIP Safe in 2026? Reality Check, Risks, Returns and Smart Investment Strategy for Indian Investors

Bitcoin SIP in 2026: Can It Really Make You Rich?… Read more: Invest in Bitcoin SIP Safe in 2026? Reality Check, Risks, Returns and Smart Investment Strategy for Indian Investors - How to Get the Best Returns from Post Office Investments in 2026: Smart Strategies to Earn Up to 9.75% Safely

When it comes to safe and guaranteed investments in India,… Read more: How to Get the Best Returns from Post Office Investments in 2026: Smart Strategies to Earn Up to 9.75% Safely

When it comes to safe and guaranteed investments in India,… Read more: How to Get the Best Returns from Post Office Investments in 2026: Smart Strategies to Earn Up to 9.75% Safely - Check this Before Start SIP for MF in 2026 : 5 Best Mutual Funds In Last 5 Years

Mutual fund investing has become one of the most effective… Read more: Check this Before Start SIP for MF in 2026 : 5 Best Mutual Funds In Last 5 Years

Mutual fund investing has become one of the most effective… Read more: Check this Before Start SIP for MF in 2026 : 5 Best Mutual Funds In Last 5 Years - Stock Market Investment for Government Employees and Pensioners: Eligibility, Rules and Tips

Concept of Invetment in Stock Market for Govt Employees and… Read more: Stock Market Investment for Government Employees and Pensioners: Eligibility, Rules and Tips

Concept of Invetment in Stock Market for Govt Employees and… Read more: Stock Market Investment for Government Employees and Pensioners: Eligibility, Rules and Tips - 60 Years Old with No Retirement Savings? Here’s How You Can Still Build Financial Security

Turning 60 with little or no retirement savings can feel… Read more: 60 Years Old with No Retirement Savings? Here’s How You Can Still Build Financial Security

Turning 60 with little or no retirement savings can feel… Read more: 60 Years Old with No Retirement Savings? Here’s How You Can Still Build Financial Security - How to Escape the Middle-Class Mindset and Become Wealthy Through Honest Efforts

Many people spend their entire lives working hard, earning decent… Read more: How to Escape the Middle-Class Mindset and Become Wealthy Through Honest Efforts

Many people spend their entire lives working hard, earning decent… Read more: How to Escape the Middle-Class Mindset and Become Wealthy Through Honest Efforts - The Best Mutual Fund Selection Strategy for Long-Term Wealth Creation: An Expert Guide for Smart Investors

How to Choose the Right Mutual Funds Using Rolling Returns,… Read more: The Best Mutual Fund Selection Strategy for Long-Term Wealth Creation: An Expert Guide for Smart Investors

How to Choose the Right Mutual Funds Using Rolling Returns,… Read more: The Best Mutual Fund Selection Strategy for Long-Term Wealth Creation: An Expert Guide for Smart Investors - Retired with a Lump Sum? Here’s the Smartest Way to Invest for Regular Income and Financial Security

Whether you are retired or serving employee of Govt/PSU/Corporate Sector,… Read more: Retired with a Lump Sum? Here’s the Smartest Way to Invest for Regular Income and Financial Security

Whether you are retired or serving employee of Govt/PSU/Corporate Sector,… Read more: Retired with a Lump Sum? Here’s the Smartest Way to Invest for Regular Income and Financial Security - Government Employees and Share Market Investment Rules in India: What Is Allowed, What Is Prohibited, and Reporting Requirements Explained

With increasing awareness about wealth creation through stocks, mutual funds,… Read more: Government Employees and Share Market Investment Rules in India: What Is Allowed, What Is Prohibited, and Reporting Requirements Explained

With increasing awareness about wealth creation through stocks, mutual funds,… Read more: Government Employees and Share Market Investment Rules in India: What Is Allowed, What Is Prohibited, and Reporting Requirements Explained - Best Investment Options for Senior Citizens in 2026: Safe Investments, High Returns & Regular Income Guide

Senior Citizen Investment Planning 2026: Where Should Retirees Invest Their… Read more: Best Investment Options for Senior Citizens in 2026: Safe Investments, High Returns & Regular Income Guide

Senior Citizen Investment Planning 2026: Where Should Retirees Invest Their… Read more: Best Investment Options for Senior Citizens in 2026: Safe Investments, High Returns & Regular Income Guide